The Rent Collector

You paid off your house. Connecticut didn’t.

A woman posted something on Facebook recently that went modestly viral in certain Connecticut circles. She bought her home for $60,000 in 2009. The county now says it’s worth $246,000. She didn’t sell it. She didn’t receive a check for $246,000. She didn’t realize any gain. But her property taxes jumped as if she had.

“This is a number someone decided on paper,” she wrote, “and now I’m being billed for it.”

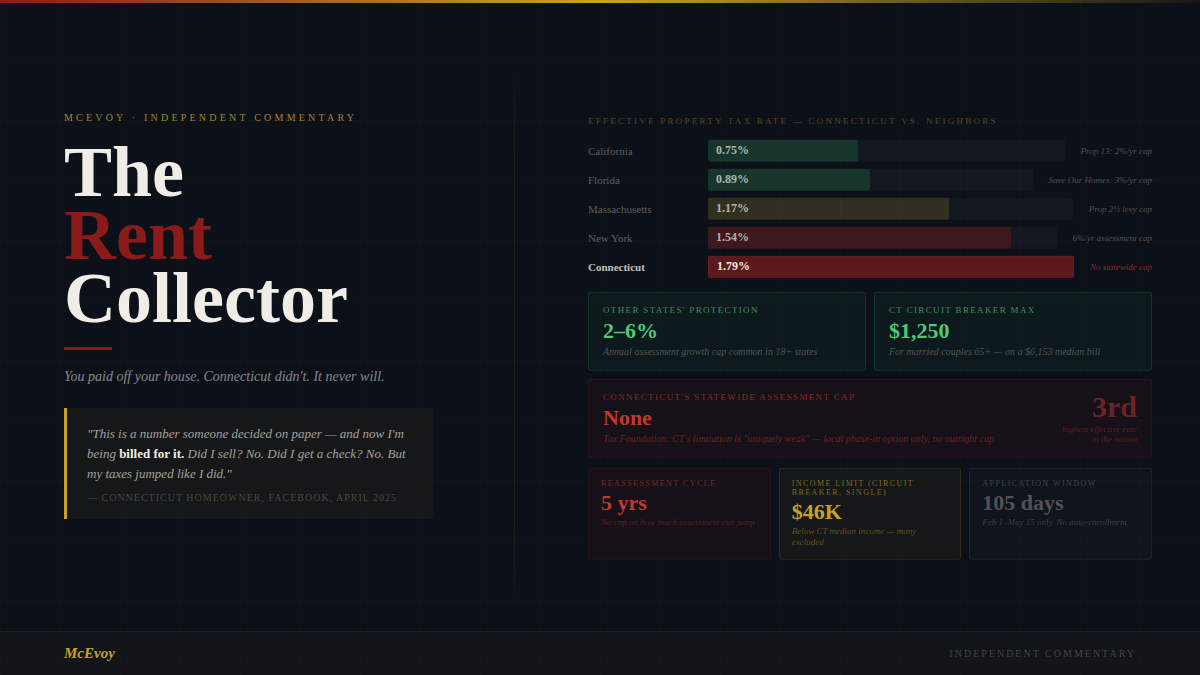

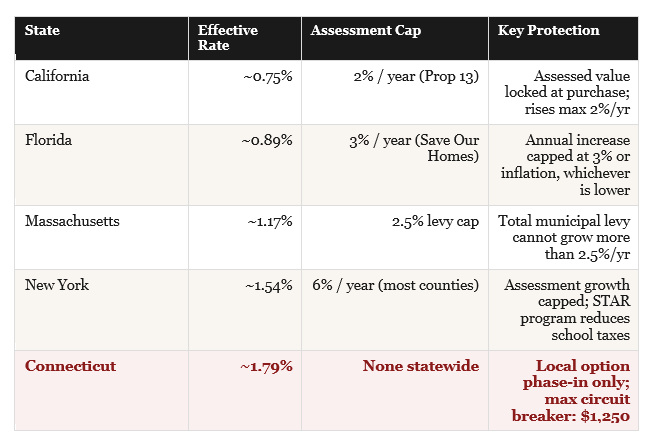

She’s right. And in Connecticut — where the property tax rate ranks third highest in the nation, where there is no meaningful cap on how fast assessments can rise, and where the circuit breaker program designed to protect vulnerable homeowners offers a maximum relief of $1,250 for a married couple — she’s more right than almost anywhere else in America.

The property tax is the closest thing in the American tax code to a pure wealth tax. It falls on an asset’s market value, not on income generated, not on gains realized, not on cash received. It arrives every year, regardless of whether the homeowner has prospered or struggled, and it does not stop when the mortgage does. You can own your home outright and still, in the most meaningful sense, never fully own it. Connecticut makes that condition more expensive than nearly any other state in the country.

The Philosophical Case — and Why It’s Mostly Right

The Facebook post framed property tax as a tax on unrealized gains, and the analogy is more than rhetorical.

Consider how the tax code treats other asset classes. If your stock portfolio doubles in value, you owe nothing until you sell. The gain is paper until realized; taxation waits for the transaction. If your business increases in value, you are not assessed annually on that appreciation. If your savings account grows, you pay income tax on the interest earned — the cash actually generated — not on the principal’s notional value.

Real property is different. It is assessed annually on its market value, and the tax bill follows that assessment regardless of whether the owner has received any income from the property, realized any gain, or has any cash with which to pay it. A retired schoolteacher who bought a modest house in Fairfield in 1992 for $185,000, paid it off over thirty years, and now receives Social Security as her primary income is sitting on a home the market values at $520,000. She has realized nothing. She has earned nothing from the appreciation. But her property tax bill has risen in approximate proportion to that paper gain, and Connecticut has provided her no meaningful automatic protection against it.

You can do everything right — pay off your home, live within your means, stay in your community for thirty years — and still find yourself squeezed out by a tax on a number someone decided on paper.

The philosophical objection goes deeper than inconvenience. Property tax is, in the language of economics, a tax on a stock rather than a flow. Income taxes tax flows — money coming in. Sales taxes tax flows — transactions occurring. Property taxes tax the accumulated value of an asset that may be generating no flow whatsoever for its owner. In that sense, the Facebook post is correct: it is structurally more similar to the “unrealized gains” wealth tax that Congress has repeatedly rejected for financial assets than it is to any conventional income or transaction tax.

The argument has a counterpart that deserves acknowledgment. Property tax is also — in its theoretical design — a charge for services rendered to the asset itself. The fire department protects the house. The roads give access to it. The schools increase its value. The courts enforce its title. A portion of the annual property tax is, in this view, not a tax at all but a fee for ongoing services that the asset directly benefits from. This is a legitimate point. It does not, however, explain why those services should cost $11,500 a year for a median Connecticut home, or why the fee should rise automatically as markets appreciate, or why a retired owner on fixed income should face the same fee structure as a wealthy family actively using all of those services.

What Connecticut Uniquely Fails to Do

Every state has property taxes. What distinguishes Connecticut is the combination of a high rate, an aggressive assessment standard, and a near-complete absence of structural protection for long-term homeowners.

Connecticut’s effective property tax rate of approximately 1.79% ranks third in the nation, behind only New Jersey and Illinois. More importantly, Connecticut has no statewide cap on how much a property’s assessed value can increase in any given reassessment cycle. The Tax Foundation describes Connecticut’s assessment limitation as “uniquely weak” — a local option for phasing in higher assessments that does not cap them outright. Eighteen other states have adopted meaningful assessment limitations. Connecticut is, in the Tax Foundation’s analysis, very nearly in the same category as the handful of states with no property tax limitations at all.

The practical consequence: when a town conducts its mandatory reassessment — required at least once every five years — homeowners can face assessment increases of 30%, 40%, or more in a single cycle, with no automatic protection. The mill rate may adjust somewhat, but there is no guarantee it will adjust enough to hold bills flat. And in Connecticut’s high-cost markets — Fairfield County, the shoreline, the Gold Coast towns — the appreciation over a five-year cycle in recent years has been dramatic.

The Circuit Breaker: A Fig Leaf on a Forest Fire

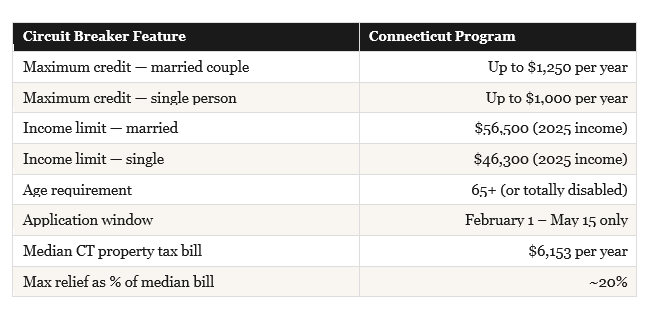

Connecticut does have a property tax relief program for elderly and disabled homeowners. It is called the circuit breaker, and it is, in the context of a state with among the highest property tax bills in the nation, almost comically inadequate.

The median Connecticut property tax bill is $6,153 per year. The maximum circuit breaker credit for a married couple is $1,250 — about 20% of the median bill. For a homeowner in Westport, Greenwich, or Darien, where property tax bills routinely exceed $15,000 to $25,000 annually, the credit is between 5% and 8% of the actual burden. It is not a circuit breaker. It is a gesture.

The income limits compound the problem. A single retiree with income above $46,300 — a figure that includes Social Security, pension payments, IRA distributions, and any other income — receives nothing. That threshold is roughly $10,000 below the median individual income in Connecticut. A significant portion of the fixed-income retirees most stressed by rising assessments are above the cutoff and below the threshold of actually being comfortable. They are too affluent to qualify for relief and too cash-constrained to absorb bill increases without consequence.

The application window — February 1 to May 15 only, with biennial reapplication required — ensures that a meaningful portion of eligible homeowners miss it every year. There is no automatic enrollment. There is no proactive outreach. The program is designed to be applied for, not found. Connecticut could automatically enroll every homeowner over 65 who files a state tax return. It has chosen not to.

Connecticut’s maximum circuit breaker credit is $1,250. The median property tax bill is $6,153. The math is not a safety net. It is a formality.

What Other States Got Right

The solutions to this problem are not theoretical. They exist, they are functioning, and Connecticut’s neighbors have implemented versions of them.

California’s Proposition 13 is the most famous and most debated. Passed by voters in 1978, it caps the annual increase in assessed value at the lesser of 2% or inflation, regardless of market conditions, until the property is sold. A homeowner who bought in Irvine in 1995 for $250,000 pays roughly $4,000 per year in base property taxes. Their neighbor who bought the identical home in 2024 for $1.1 million pays approximately $11,000. The long-term owner is protected from paper appreciation. Prop 13 has real drawbacks — it creates inequities between neighbors, discourages mobility, and shifts burden toward renters and commercial property — but the protection it provides to long-term homeowners on fixed incomes is genuine and effective.

Massachusetts’ Proposition 2½ takes a different approach. Rather than capping individual assessments, it caps the total property tax levy a municipality can raise at 2.5% of the total assessed value of all property, and limits annual levy growth to 2.5%. The effect is that even when individual property values rise sharply, the total tax collected by the town cannot grow faster than 2.5% without a public override vote. Massachusetts went from property taxes 76% above the national average before Prop 2½ to only 13% above it within five years of passage. Connecticut has no equivalent.

Florida’s “Save Our Homes” caps annual increases in assessed value for homestead properties at the lesser of 3% or the Consumer Price Index. The cap is portable — when a Florida homeowner sells and buys another home, they can carry their accumulated savings to the new property, eliminating the “lock-in effect” that traps California homeowners in homes they might otherwise sell.

Connecticut has none of these. What it has is a local option to phase in large assessment increases over time — meaning the increase is still fully absorbed, just spread across more years. The destination is the same. The pain is merely staged.

The Fix Connecticut Won’t Discuss

The solutions are available, well-tested, and politically achievable. The obstacle is not knowledge or capacity. It is the institutional resistance of a municipal finance system that depends on unconstrained property tax growth to fund ever-expanding local budgets.

Three changes would materially address the problem without requiring Connecticut to become California: a meaningful assessment growth cap, an expanded and automatic circuit breaker, and a genuine freeze option for long-term elderly homeowners.

An assessment growth cap of 3–5% annually — similar to Florida’s Save Our Homes model — would protect long-term homeowners from sharp valuation spikes while still allowing municipalities to capture gradual market appreciation. Critically, the cap should reset to market value on sale, so the protection accrues to the resident rather than being inherited by the buyer. This addresses the fairness objection while preserving the protection for the people who actually need it.

Automatic circuit breaker enrollment for every homeowner over 65 who files a Connecticut state income tax return, with income thresholds raised to at least the state median income and credits scaled to actual tax burden rather than fixed at $1,000–1,250 regardless of the bill. A credit capped at $1,250 against a $15,000 bill is not relief. A credit equal to 50% of the amount above, say, 5% of household income would be.

A property tax freeze for homeowners over 75 with long-term residency — say, ten or more years in the same property — and income below 150% of the state median. The freeze holds the bill at its current level for as long as the homeowner remains in the property, with the deferred appreciation captured at sale. The homeowner stays. The town eventually gets its money. Nobody gets taxed out of their home.

None of these proposals require the state to forgo revenue permanently. They require it to defer some portion of revenue until a transaction occurs — exactly the model the entire rest of the tax code uses for unrealized gains.

The Real Answer to the Facebook Post

The woman who posted on Facebook was making a genuine and philosophically defensible point. She is being taxed on wealth she has not realized, cannot access, and did not choose to create. She is paying, annually and in cash, for an appreciation that exists only on a county assessor’s worksheet. If she sells, she’ll owe capital gains tax on that gain too — meaning it will be taxed twice, once annually as assessed value and again upon realization.

The counterarguments — that property tax funds real services, that she benefits from her home’s appreciation, that programs exist to help — are all partially true and none of them fully answer the question she’s actually asking, which is: why is real property the only major asset class in America that gets taxed annually on its unrealized market value, with no cap, no automatic protection, and a relief program whose maximum benefit wouldn’t cover two months of the average Connecticut homeowner’s bill?

Connecticut has a specific version of this problem that is worse than almost anywhere else: the highest effective rate in New England, no meaningful assessment cap, a circuit breaker that is underfunded and underutilized, and a political system that has consistently chosen to protect municipal revenue over homeowner stability.

You paid off your house. Connecticut didn’t. It will keep collecting its share indefinitely, reassessing the value every five years, sending the bill every year, regardless of whether you sold anything, earned anything, or received anything at all. The mortgage ends. The tax bill does not.

— McEvoy —

Sources: Tax Foundation (“What Can Connecticut Learn from its Neighbors About Property Tax Limitations?”); Kiplinger State Property Tax Rankings 2026; CT Office of Policy and Management (Circuit Breaker Program); CT General Assembly OLR Report 2026-R-0027; Lincoln Institute of Land Policy; California State Board of Equalization (Prop 13); Florida Save Our Homes statute; USAFacts; Connecticut General Statutes §§12-170aa.

The issue with assessments is that the increase or decrease in the value of your home can be lumpy based on where your home is located in your town. So if “in town” walkable living becomes more desirable, the homes near downtowns increase in value more than those further away from the downtown. Also impacting assessments is the value of commercial property. When the state has anti-business policies as it has been passing for decades now, that makes it uneconomical for businesses to be in the state and they end up leaving, along with their good paying jobs. Commercial buildings go vacant, producing little commercial revenues for the municipality. When this happens, the value of residential land becomes higher than the value of commercial land. So the residential property taxes become higher part of the mix while commercial taxes are lower. These “lumpy” changes in property values are what cause real shocks to homeowners paying taxes when the assessments are done every 5 years. If the valuations all went up equally for both commercial and residential with price inflation, the mill rate would go down by an equal measure, and real dollar taxes would be flat, except for any annual increase in the municipality’s yearly budget. So these are two separate factors that are responsible for the increase in taxes post a revaluation: 1) the mix of commercial vs residential property values and pricing differences by location within a municipality and 2) the annual municipal budget increase. You must consider at the effects of state legislative policy making to understand the impacts on commercial businesses in CT. Further, policies like the "as of right" summary review conversions of commercial to residential passed in HB8002 in November 2025, which goes into effect on 7/1/2026 will also have enduring impacts on local property taxes. If a commercial property is converted to residential, those commercial revenues are gone forever and local property taxes will be more heavily relied upon to meet municipal budget increases. Note: When comparing CT to FL it is also important to note that FL reassessments on properties are done YEARLY, not every 5 years. Our 5 year assessments make those hard and fast rules more complicated. Converting to annual assessment revaluations would be yet another costly unfunded mandate on municipalities, but it would prevent the sudden shocks we see with the every 5 year revaluations.